|

|

|

Effective Information & Strategy |

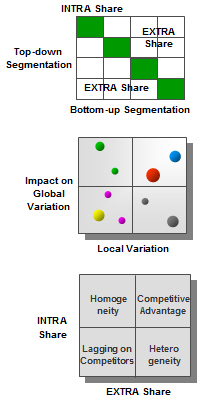

Managing Intra & Extra share... for increased competitive advantageThe concepts of Intra and Extra share cannot be avoidedWhether an analysis is based on a single Key Performance Indicator (KPI) or on a matrix of KPIs, the total Extra share of a segmentation measures its relevance to the chosen KPI(s). It is always tempting to seek the most homogeneous segmentation possible, ideally without any Extra share. And the MBA approach provides for the building, given any base segment, of an homogeneous segmentation. But that is only possible for a single point of view and given time period. When working with multiple viewpoints, concepts of Intra and Extra shares simply cannot be avoided. Today's agile enterprise needs to be managed with Extra shareThe existence of Extra shares and their inherent heterogeneity, are not necessarily limits to sound management. To the contrary, Extra share often provides for flexibility and leverage, taking into account structural changes due to changes in mix: a product may have declined in margin percent, and yet have a positive impact on overall margin. Managing with homogeneous segments may result in vertical organizations that often do not account for transverse dynamics between markets, customers and products. The agile organization requires Extra share in its management structures. Too much Extra share may prove unstableToo much Extra share might lead to a chaotic situation. But its presence is unavoidable with rapid fluctuations of the current business environment, and ignoring or avoiding it may be sterile if not dangerous. Learning to measure and integrate Extra share into decision-making processes, is best taming it; and potentially finding new sources of competitive advantage. Indeed, all traditional methods of business management, from cost accounting to marketing and organizational design, tend to minimize or eliminate the presence of Extra share. A legacy that still carries its burden today. |

|

|

| . | ||

| Copyright 1989-2014 EFFIS | ||